Just exactly who are these union busters?

Surprisingly, there is a lot of information to be gleaned from Form LM-20 about the individuals who plan and run captive audience meetings, follow employees around the workplace asking questions, and otherwise “persuading.”

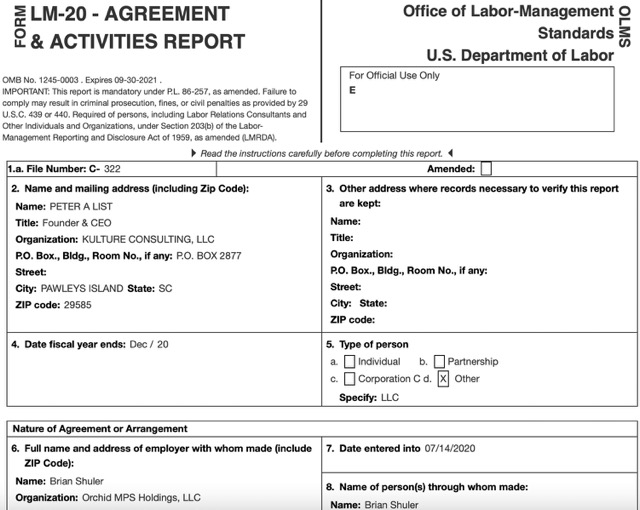

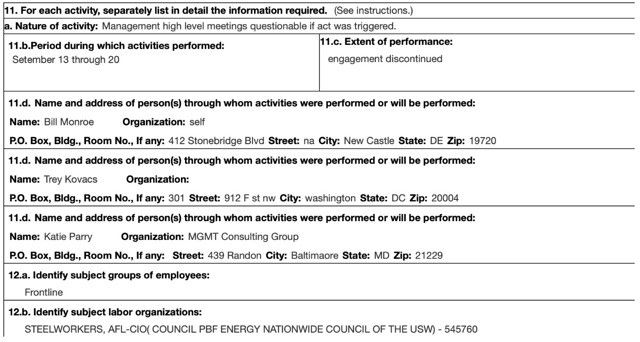

Form LM-20 (shown below) is used by consultants to report persuader agreements and arrangements within thirty days of entering one with an employer. Besides information about the persuader and the employer, the date, nature and other details of the agreement, the persuader is supposed to report the full names, organizational affiliation and address of the individuals doing the persuading in item 11(d).

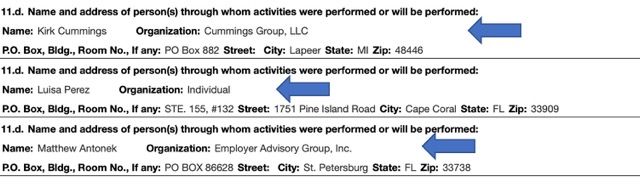

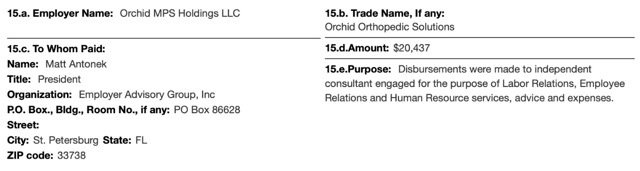

In this LM-20 filed by Kulture for Orchid MPS Holdings, the names of three individuals (highlighted by blue arrows below) and their organizational affiliations are given in §11(d) excerpted below:

While Kulture is the persuader named in this LM-20 form, §§11(d) tells us that none those who will or have performed the persuader activities are employees of Kulture; if they were, their “organization” would have been identified as “Kulture” but as can clearly be seen, it is not. Instead, these three individuals are subcontractors: Cummings is employed by the Cummings Group, Perez is self-employed and Antonek is employed by Employer Advisory Group.

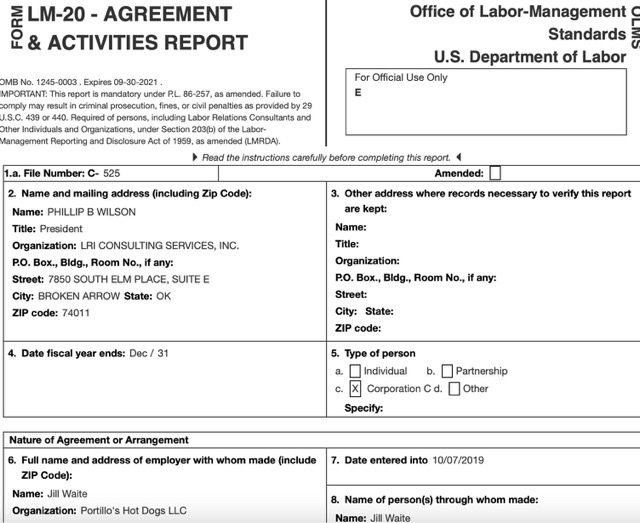

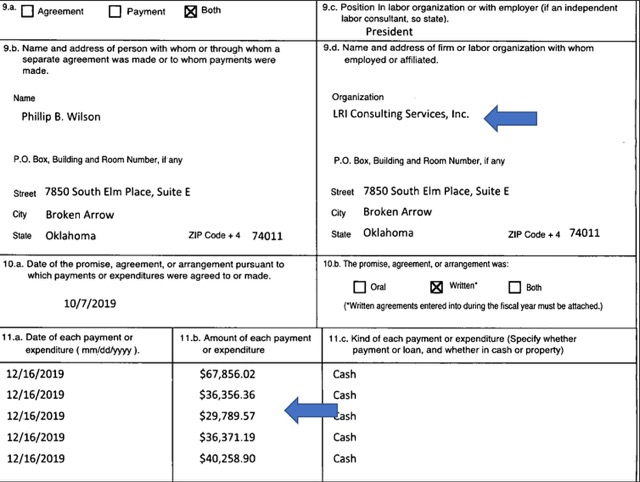

Exactly how common is this practice of subcontracting out persuader work? While the exact numbers are not yet known, LaborLab has recently compiled two years’ worth of LM-20s (from 1/1/2021 through 12/31/2022) and has begun to take a closer look. Here is another example of persuader subcontractors named in item 11(d), this time in an LM-20 filed by LRI.

The instructions for Part D indicate the persuader must report in items 15 and 16, disbursements to persons “other than officers and employees of the reporting organization” where the purpose of the payment is for reportable persuasion activities (in other word, subcontractors). Obviously, if the individuals are listed as subcontractors in item 11(d) of the LM-20, these payments are for reportable persuader activities and because an organization other than the persuaders is listed as their employer, they are obviously subcontractors. It should be further pointed out that these subcontractors are also obligated to file their own Form LM-20 and their own Form LM-21 at the end of their fiscal year.

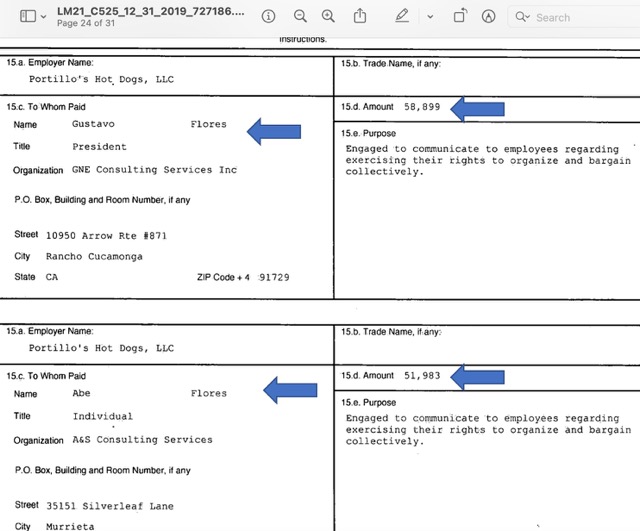

The arrangement was reported in 2019 according to item 7 of the LM-20 and using the OLMS Public Disclosure website, we obtained the LM-21 for LRI for 2019. Below, we show that LRI did indeed itemize payments to these two subcontractors, Gustavo and Abe Flores. Note that both show the employer’s name in item 15(a), and in 15(c) the names and organizations and the total 2019 payments to each subcontractor.

Completing the loop, the employer, Portillo Hot Dogs, should have also filed an LM-10 for 2019 and itemized total payments to the prime contractor, LRI. In the screen print below, Portillo’s 2019 LM-10 reflects persuader payments to LRI (not just to the subcontractors).

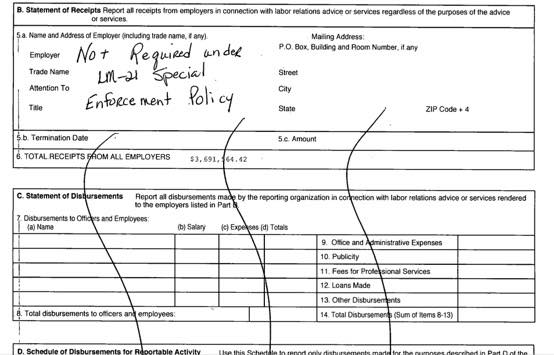

The total payments reported by Portillo Hot Dogs to LRI total $210,632. Total payments shown on the LM-21 by LRI to Gustavo and Abe Flores together total $110,882. When subtracting total payments to the two listed subcontractors, $110,882, from total payments to the persuader from the employer, $210,632, the difference is nearly $100,000. Because persuaders are not required to complete Parts B and C of Form LM-21 under the OLMS “Special Enforcement Policy, we have no idea if there were other payments made by LRI for other expenditures. In fact, in their 2019 LM-21 shown in the screen print below, LRI specifically cited the OLMS Special Enforcement Policy.

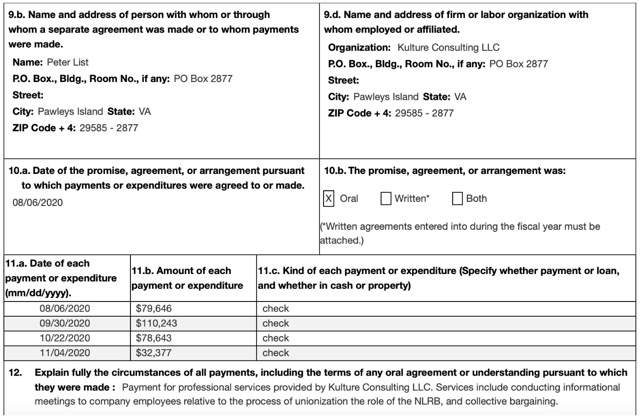

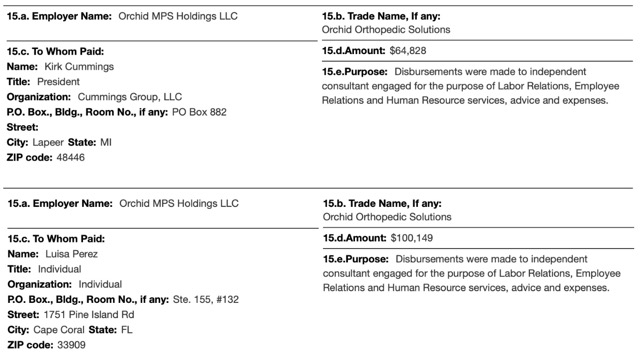

Here is the 2020 LM-10 filed by Orchid showing total persuader payments to Kulture.

Total payments from Orchid to Kulture from the LM-10 form above are $300,909. Here are the itemized statements (items 15 and 16 from Kulture’s 2020 Form LM-21. Payments to these three subcontractors total $185,414, compare with total payments from the employer, Orchid, to Kulture, of $300,909.

While this analysis is certainly illuminating, we need more details. If the Special Enforcement Policy on Form LM-21 were rescinded, persuaders would have to reveal all disbursements, not just those to persuader subcontractors, as well as all receipts. Additionally, in 2021, nearly half of the consultants who should have filed an annual report (Form LM-21) have not yet done so. And a significant number of employers identified by Form LM-20s, have not yet filed their 2021 LM-10s. Our ability to repeat this kind of analysis is somewhat limited.

LaborLab is committed to total transparency of the persuader industry and the employers who hire them. While the OLMS Public Disclosure database is a positive step forward, it doesn’t allow you to easily conduct the kind of analysis shown here. However, we are soon putting up our 2021-2022 LM-20 database online so you will be able to search all the individuals and organizations, the persuaders and employers they have worked for in the calendar year 2021-2022 period.

In a recent post, LaborLab revealed that former OLMS Special Assistant Trey Kovacs had worked as a union buster at JSW Steel.

In our database, you’ll be able to select any name from a dropdown list (including Trey Kovacs, as shown here) and display their reported work for the last two years.

And for each entry you find, there will be a hyperlink to the LM-20, so you can pull it up for documentation purposes.

Watch this space!